Admin Process Concepts

The following is for entertainment/educational purposes and is not to be construed as the practice of law of any kind. This is not a “Debt Relief Service” of any kind.

There are Seven Main Concepts that will help make the administrative procedure make sense to a “layperson” with no previous experience. All the supported evidence and case law, maxims of law, etc, are provided with links below each concept, for your further study if you should so choose:

Using a Private Administrative Process, you can get a lawfully binding contract with a debt collector, bank (for credit card), mortgage company, any State or Municipality (including the USA), any party with beef who might sue you, IRS, or even your ex-spouse who you want to work out a fair divorce with.

You can use this to get any company to Cease and Desist, stop collection attempts, reverse a lien/levy/garnishment, and basically to go away and resolve the issue entirely. Please familiarize yourself with the following concepts:

Concept One: There is No Money

In our society today, due to the major Bankruptcy in 1933, [look up “HJR 192”], all “money” is debt, not assets. It is even printed right on the front of all Federal Reserve Notes “This Note is Legal Tender For All Debts, Public And Private.”

In the past, US Dollars were actually based on Gold or Silver and was merely a receipt which could be exchanged for this real money of substance.

So now, you have realized that no asset of any value was loaned to you. What is really happening is that your signature on a loan application is what authorized the bank to access your own credit, which is unlimited in your lifetime, based off your birth certificate (which is a bond).

Credit is created through bonds, promises to pay, and based on the commercial energy of the living person whose autograph/signature is affixed to the document. Strictly speaking, when you sign the loan application, you are placing a lien on the birth certificate, which is an asset also the Title to your body or your physical person. You are an asset and you are the source of the money. The piece of paper with your signature is now a security, and has value to it. You are exchanging that note (an asset) for debt (as “Credit”).

The banks only deal in Credits and Debit based on book entries. Look in your online banking or the paper statements that you get in the mail – the only two ledgers you see are “Debits” and “Credits”. Nowhere does it say “Money”.

In addition, it is now public policy (Public Law 7310) that the “payment of debt” is now against Congressional and “public policy” and henceforth, “Every [debt] obligation . . . Shall be discharged.” What this means is that you can send your bills to the United States Treasury or the IRS (their auditor), and they will discharge or “set off” your debt with your unlimited credit. This is a process that is explained on our website, it is called “Accepted for Value”. However for the majority of people, this procedure is not recommended until one recognizes the inherent power that they have and is responsible enough to do the procedure effectively. For novices to this information, we do not recommend an Accepted for Value procedure to settle a Credit Card debt. There are many ways to accomplish the same goal – you not being liable for a debt and to avoid any lawsuits/judgments and to clean up your credit. We usually talk with our client to discuss the best procedure for their unique situation – however all procedures will use all seven of these concepts listed on this webpage.

As a result of HJR 192, and from that day forward (June 5, 1933), no one in this nation has been able to lawfully pay a debt or lawfully own anything. The only thing one can do, is tender in transfer of debts, with the debt being perpetual. The suspension of the gold standard, and prohibition against paying debts, removed the substance for our common law to operate on, and created a void as far as the law is concerned. This substance was replaced with a “PUBLIC NATIONAL CREDIT SYSTEM” where debt is “LEGAL TENDER” money.

192 states that one cannot demand a certain form of currency that they want to receive if it is dollar for dollar. If you review the Modern Money Mechanics article you will discover that all currency is your credit! The Federal Reserve calls it “monetized debt.”

How Money Is Created (1 of 3): http://www.youtube.com/watch?v=AgKFLk9xffA&feature=fvwrel

Modern Money Mechanics – Federal Reserve Bank of Chicago

http://www.rayservers.com/images/ModernMoneyMechanics.pdf

House Joint Resolution 192 (1933) / Public Law 7310 – Remedies in Law:

http://www.scribd.com/doc/72416275/HJR-192-Original-1933-06-05

http://www.youtube.com/watch?v=IN4QFJPPbWA

Concept Two:

An Unrebuted Affidavit Stands as Truth in Commerce:

For Demand or Proof of the Debt, the banks have never responded to our inquiry properly. Therefore they consent to our Affidavit of Facts and our New Contract.

“If only one side of the conflict was supported by affidavit, our task would be relatively easy, for we may not assume the truth of allegations in a pleading which are contradicted by affidavit.” -Taylor v. Portland Paramount Corp., 383 F.2d 634, 639 (9th Cir. 1967).

“Where affidavits are directly conflicting on material points, we do not see how it is possible for the district judge to “weigh” the affidavits in order to resolve disputed issues. Except in those rare cases where the facts alleged in an affidavit are inherently incredible, and can be so characterized solely by a reading of the affidavit, the district judge has no basis for a determination of credibility.” -Data Disc, Inc. v. Systems Technology Associates, Inc. -United States Court of Appeals, Ninth Circuit, July 13, 1977

Video: http://www.youtube.com/watch?v=Eg8GuY1cy_g

Concept Three:

A Request Regarding an Authenticated Statement of Account:

This International Commercial Law basically shows that a debt is considered discharged if the debt collector / original “Creditor” fails to reply and rebut your Affidavit of a Zero Balance. This is yet another process we use to demand proof of any authentic debt, which the banks/debt collector never properly respond to.

UCC 9210:

(1) A debtor may sign a statement indicating what he believes to be the aggregate amount of unpaid indebtedness as of a specified date and may send it to the secured party with a request that the statement be approved or corrected and returned to the debtor. When the security agreement or any other record kept by the secured party identifies the collateral a debtor may similarly request the secured party to approve or correct a list of the collateral.

(2) The secured party must comply with such a request within two weeks after receipt by sending a written correction or approval. If the secured party claims a security interest in all of a particular type of collateral owned by the debtor he may indicate that fact in his reply and need not approve or correct an itemized list of such collateral. If the secured party without reasonable excuse fails to comply he is liable for any loss caused to the debtor thereby; and if the debtor has properly included in his request a good faith statement of the obligation or a list of the collateral or both the secured party may claim a security interest only as shown in the statement against persons misled by his failure to comply. If he no longer has an interest in the obligation or collateral at the time the request is received he must disclose the name and address of any successor in interest known to him and he is liable for any loss caused to the debtor as a result of failure to disclose. A successor in interest is not subject to this section until a request is received by him.

(3) A debtor is entitled to such a statement once every six months without charge. The secured party may require payment of a charge not exceeding $10 for each additional statement furnished.

http://www.law.cornell.edu/ucc/9/9-208.html

http://www.youtube.com/watch?v=NauEHmyascY

Concept Four:

Fair Debt Collection Practices Act and the Duty of a Debt Collector to Validate a Debt when Demand is Made:

More public law to support consumers and our efforts at validating the debt:

http://www.ftc.gov/os/statutes/fdcpa/fdcpact.shtm#809

§ 809. Validation of debts [15 USC 1692g]

(a) Within five days after the initial communication with a consumer in connection with the collection of any debt, a debt collector shall, unless the following information is contained in the initial communication or the consumer has paid the debt, send the consumer a written notice containing —

(1) the amount of the debt;

(2) the name of the creditor to whom the debt is owed;

(3) a statement that unless the consumer, within thirty days after receipt of the notice, disputes the validity of the debt, or any portion thereof, the debt will be assumed to be valid by the debt collector;

(4) a statement that if the consumer notifies the debt collector in writing within the thirty-day period that the debt, or any portion thereof, is disputed, the debt collector will obtain verification of the debt or a copy of a judgment against the consumer and a copy of such verification or judgment will be mailed to the consumer by the debt collector; and

(5) a statement that, upon the consumer’s written request within the thirty-day period, the debt collector will provide the consumer with the name and address of the original creditor, if different from the current creditor.

(b) If the consumer notifies the debt collector in writing within the thirty-day period described in subsection (a) that the debt, or any portion thereof, is disputed, or that the consumer requests the name and address of the original creditor, the debt collector shall cease collection of the debt, or any disputed portion thereof, until the debt collector obtains verification of the debt or any copy of a judgment, or the name and address of the original creditor, and a copy of such verification or judgment, or name and address of the original creditor, is mailed to the consumer by the debt collector.

(c) The failure of a consumer to dispute the validity of a debt under this section may not be construed by any court as an admission of liability by the consumer.

Concept Five:

Tacit Acquiescence is Acceptance:

http://legal-dictionary.thefreedictionary.com/acquiescence

This explains to you how we get the companies to “Agree” with our new contract that the debt is settled/discharged/zeroed out:

Definition of “Tacit Acquiescence”: Conduct recognizing the existence of a transaction and intended to permit the transaction to be carried into effect; a tacit agreement; consent inferred from silence.

For example, a new beer company is concerned that the proposed label for its beer might infringe on the trademarkof its competitor. It submits the label to its competitor’s general counsel, who does not object to its use. The new company files an application in the Patent and Trademark Office to register the label as its trademark and starts to use the label on the market. The competitor does not file any objection in the Patent Office. Several years later, the competitor sues the new company for infringing on its trademark and demands an accounting of the new company’s profits for the years it has been using the label. A court will refuse the accounting, since by its acquiescence the competitor tacitly approved the use of the label. The competitor, however, might be entitled to an Injunction barring the new company from further use of its trademark if it is so similar to the competitor’s label as to amount to an infringement.

Similarly, the Internal Revenue Service (IRS) may acquiesce or refuse to acquiesce to an adverse ruling by the u.s. tax court or another lower federal court. The IRS is not bound to change its policies due to an adverse ruling by a federal court with the exception of the U.S. Supreme Court. The chief counsel of the IRS may determine that the commissioner of the IRS should acquiesce to an adverse decision, however, thus adopting the ruling as the policy of the IRS. The decision whether to acquiesce to an adverse ruling is published by the Internal Revenue Service as an Action on Decision.

Acquiescence is not the same as Laches, a failure to do what the law requires to protect one’s rights, under circumstances misleading or prejudicing the person being sued. Acquiescence relates to inaction during the performance of an act. In the example given above, the failure of the competitor’s general counsel to object to the use of the label and to the registration of the label as a trademark in the Patent and Trademark Office is acquiescence. Failure to sue the company until after several years had elapsed from the first time the label had been used is laches.

Concept Six:

Contracts Can Move & “Holding Your Contract”:

You have already probably received “New Terms” for your credit card, or Notices of new terms for collecting unemployment amounts or social security amounts, etc. Any contract can change and this is supported and agreed by the other party if the other party does not respond in order to re-negotiate those proposed new terms. Within 72 hours (actually 10 days – for mail to go to and fro), a new contract is agreed upon if you fail to respond. However our process is allowed to change old contracts using another concept called “Nunc pro tunc” Latin for “Now For Then”. Any contract can move or be changed. The following audios are great examples, although they are lengthy they will really help to understand this concept:

http://www.cic-root.com/living-temple/CIC-Living-Temple-201002-01.mp3

http://recordings.talkshoe.com/TC-37960/TS-253362.mp3

Basically, we just want you to understand that we are moving the contract from what was once a agreed upon obligation (because of our conduct – you were paying it weren’t you?!), to now being an unsubstantiated or frivolous claim that has been rebutted by law.

Concept Seven:

Certificate of Non-Performance (also known as Dishonor):

This explains the actual Paperwork “Process” that we use:

Within the Uniform Commercial Code (UCC) is a process called a ‘Notary Certificate of Default Method” (Notary COD method). This has generally been used by banks in their commercial transactions, but more recently, the Notary COD method has been used in disputes with government agents, agencies, banks, and corporations by people who are unable to afford the services of an attorney and/or have been disappointed when seeking justice through the courts. It can be used to head off potential litigation, settling of the case prior to it’s being brought into court, or sometimes, for a case that is already in the court. It is a process of re-presentation of commercial documents that were previously presented and ignored, in order to gain response and satisfaction of your claim/inquiry.

The COD is a 3-step process which is performed by a notary after you have made a good faith effort to settle the matter with your opponent. You then bring the matter to the notary and request s/he re-present your documents to your opponent as a third party witness to their dishonor. The notary invites them to respond to him/her within a specific time frame, offering a follow-up Notice if there is no response. If no answer is forthcoming, then a Certificate of Dishonor / Non-Performance is issued.

If the Respondent fails to reply to your Presentment, or replies but does not answer your questions or provide the proof you requested or, if you request performance (like returning your property) and they do not answer or refuse for no good reason (both are ‘dishonors’), you can then bring the issue to a notary who is familiar with the COD method. The notary will re-submit your offer and/or ask the adversary why s/he is dishonoring your offer (the affidavit, contract, or whatever). Generally, the notary will contact the Respondent twice, each time giving them a specified time frame in which to answer. If no response is received, then the notary will issue a Certificate of Dishonor, the original of which is sent to you, along with copies of all of the documents in the process, and can be brought before a judge for a Declaratory Judgment or used as the basis for a lien.

We contract with others who have been trained who can help you with your COD. Contact us for more information.

Concept Eight:

Due Process:

This explains how when Due Process/Proper Notice is given in your proceeding (paperwork process), that you are giving them all Equal Protection and the right to default, acquiesce or contest:

“…due process requires, at a minimum, that an individual be given a meaningful opportunity to be heard prior to being subjected by force of law to a significant deprivation. After noting that “[t]he formality and procedural requisites for the hearing can vary, depending upon the importance of the interests involved and the nature of the subsequent proceedings,” the Boddie court continued: “That the bearing required by due process is subject to waiver, and is not fixed in form does not affect its root requirement that an individual be given an opportunity for a hearing before he is deprived of any significant property interest….” (Original italics; 401 U.S. at pp. 378-379 [28 L.Ed.2d at p. 119].) Again the court cited Sniadach as authority for the latter, general proposition. (See also Bell v. Burson (1971) 402 U.S. 535, 539-543 [29 L.Ed.2d 90, 94-97, 91 S.Ct. 1586].)

“In the latter case, we said that the right to be heard “has little reality or worth unless one is informed that the matter is pending and can choose for himself whether Page 395 U. S. 340 to appear or default, acquiesce or contest.” [Sniadach v. Family Finance Corp]

http://supreme.justia.com/cases/federal/us/395/337/case.html

If you need help with starting an administrative process, we suggest you set up a consultation on the right-side of the website!

The administrative process can be helpful pre-lawsuit (pre-foreclosure suit, pre-credit card lawsuit), or during the lawsuit process (after you’ve got a summons to answer to court). You can also attempt to resolve it AFTER you lost and have a Judgment, but the process is MUCH harder once you have a Judgment.

For more information contact – 505-340-3632

www.UnderstandContractLawAndYouWin.com

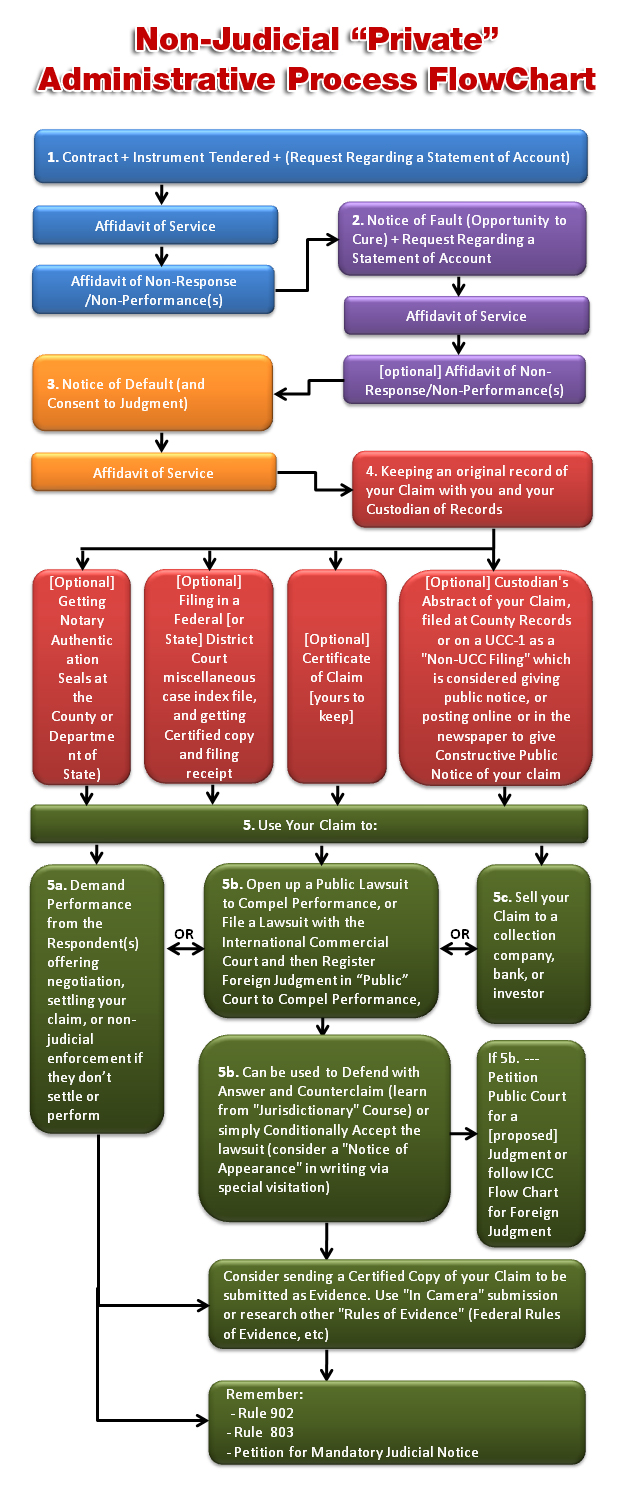

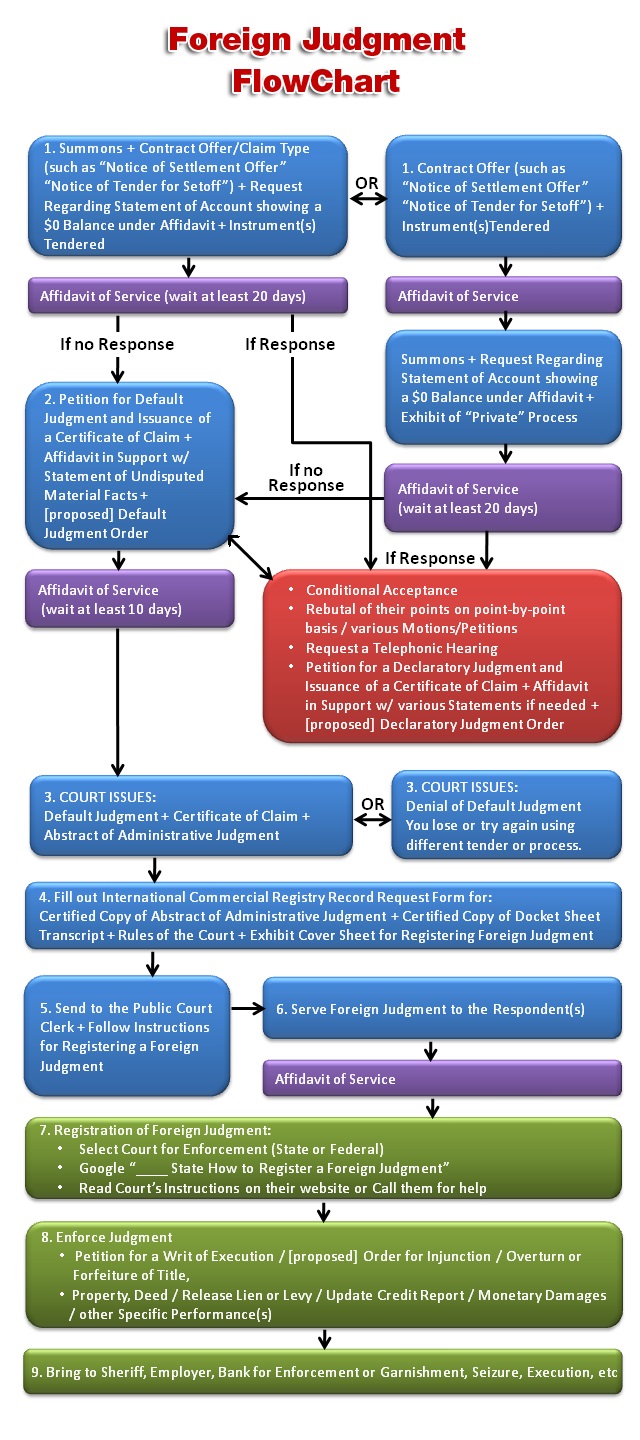

BELOW: Here are our Outlines for the Two Distinctly Different Administrative Processes.

You can discuss on a consultation the pros/cons (our opinion) of doing the Non-Judicial Admin. Process vs. the Foreign Judgment Process. Inquire by calling 505-340-3632, firstly to evaluate if this is something our experts are available to assist you with, and secondly, we’ll provide instructions on paying for consultation with Tyler or another one of our experts.