Discharging Debt with HJR 192

Discharge Debt Audios

Part 1 of 3 — Lesson on Discharging Debt with HJR 192 Remedy (Compared to Other Debt Elimination Methods)

Part 2 of 3 — Discharging Debt

Part 3 of 3 — Discharging Debt

How to Get More Free Audio Lessons

Discharging Debt with HJR 192 Remedy as an SPC (Secured Party Creditor) Success Examples:

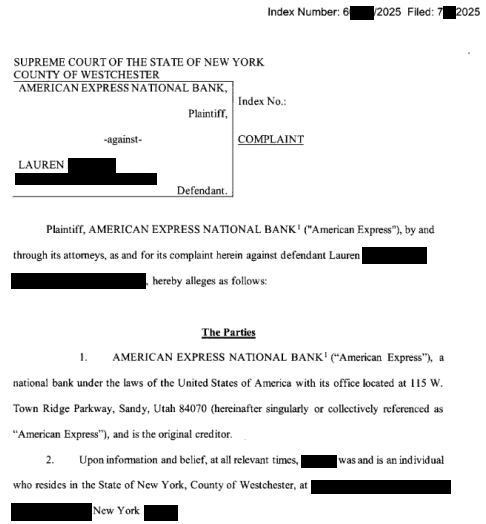

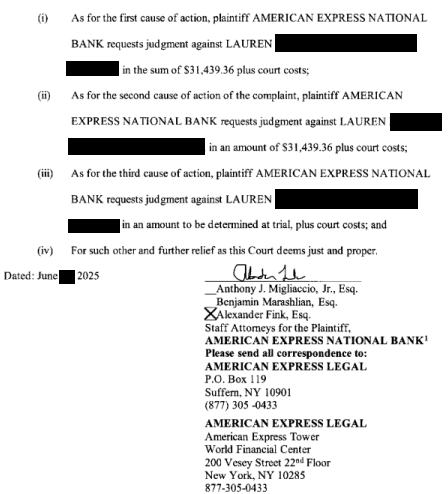

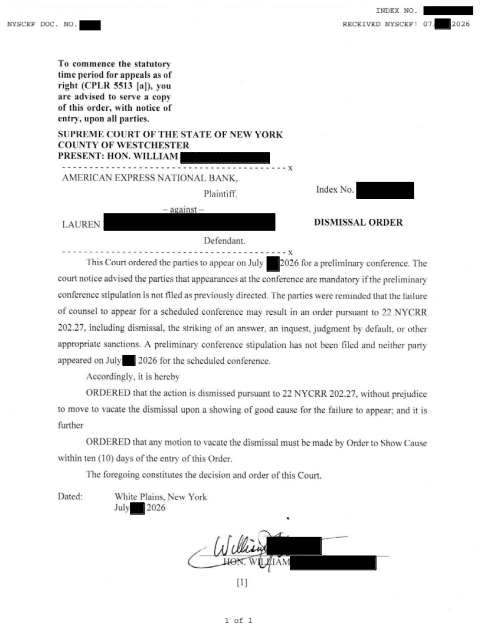

July 2016 $31,000+ Lawsuit Discharge (original – Amex balance) with SPC and HJR-192:

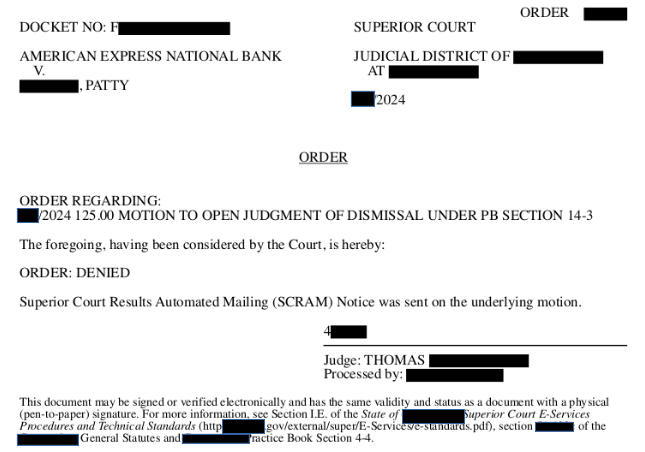

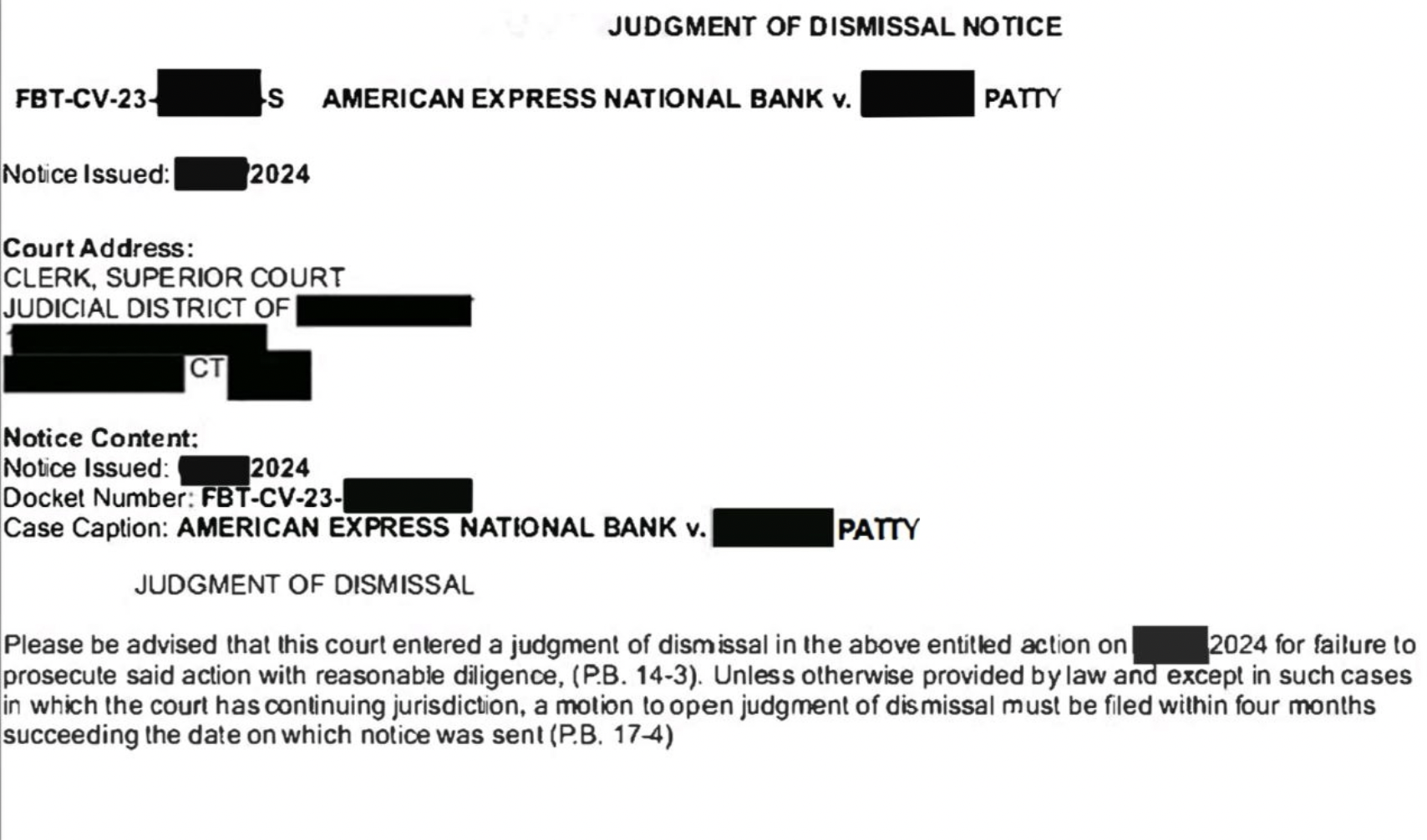

2024 $22,000+ Lawsuit Discharge (original – Amex balance) with SPC and HJR-192:

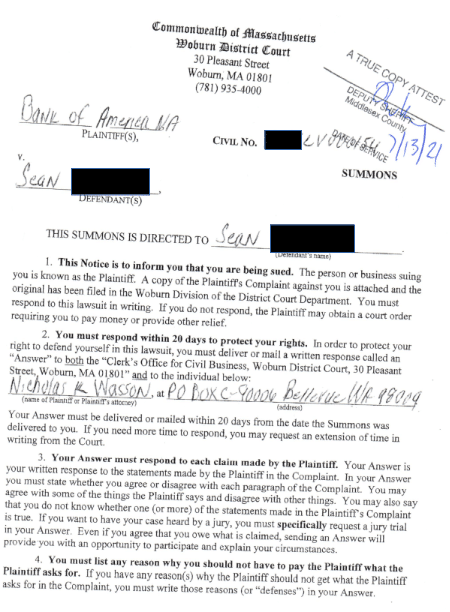

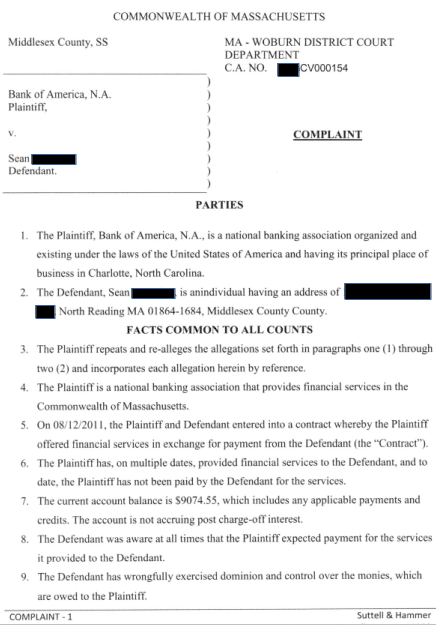

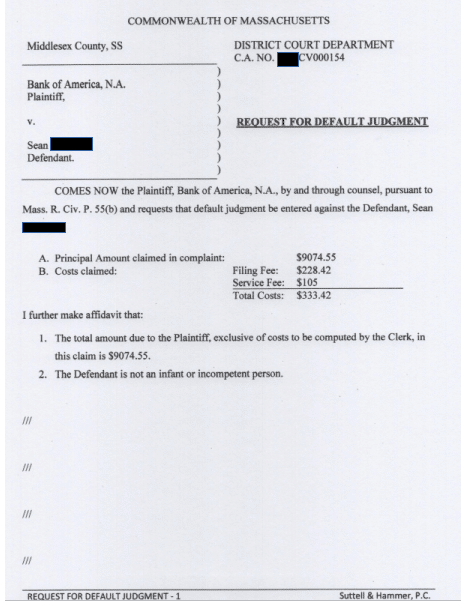

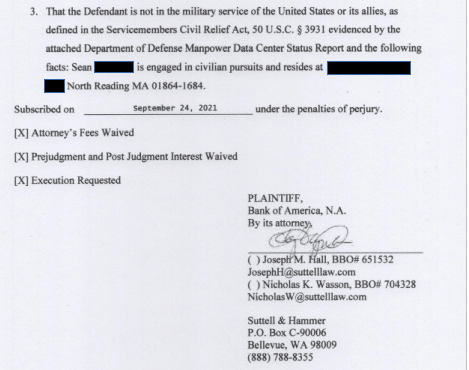

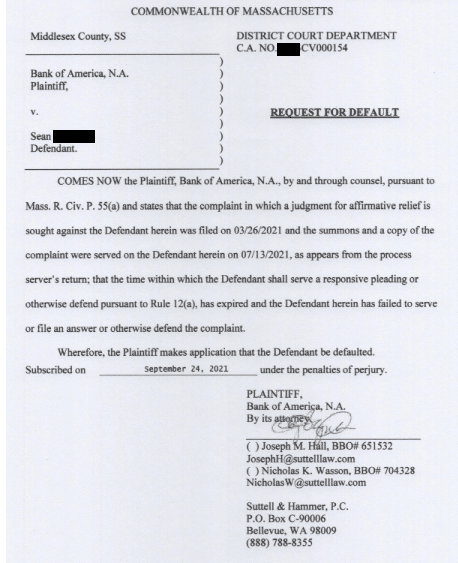

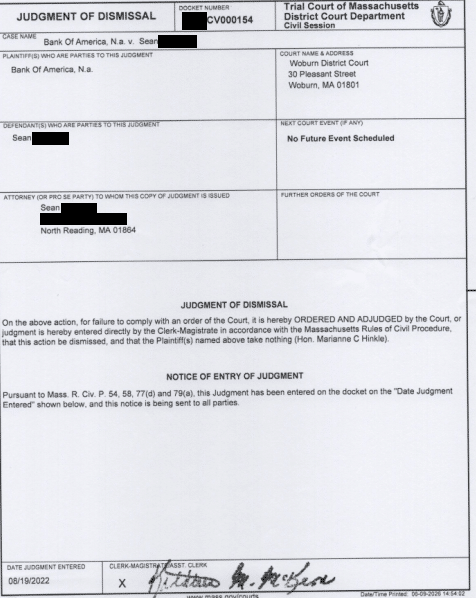

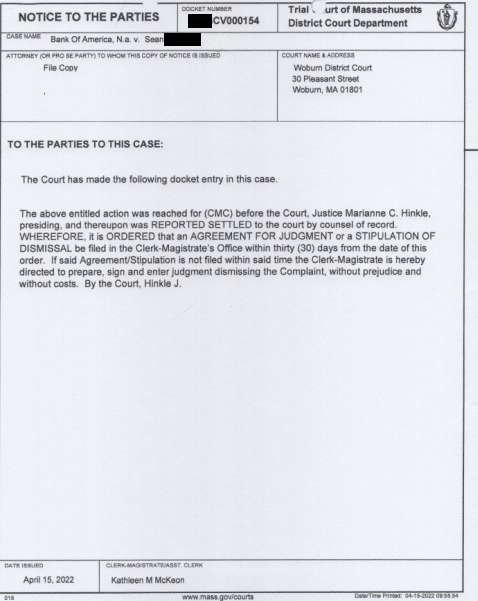

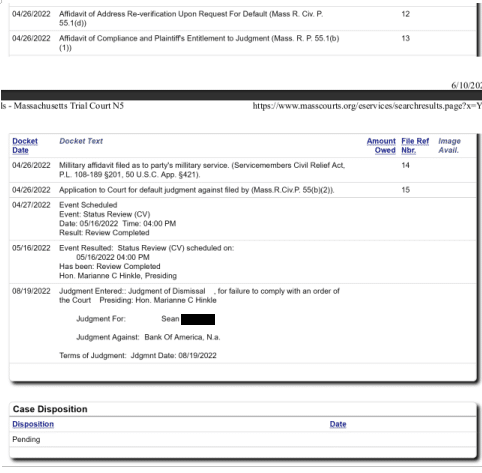

2021 Bank of America $9K+ balance Lawsuit SPC Discharge win:

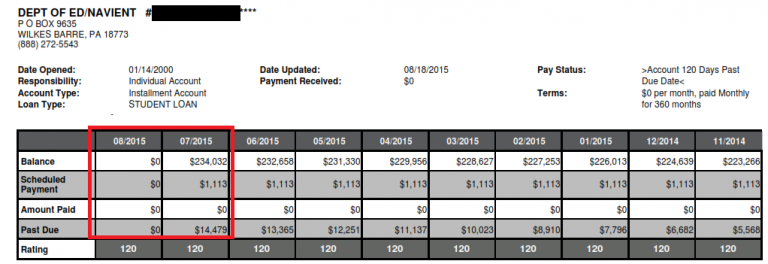

Department of Education $230,000+ Student Loan Discharge Win:

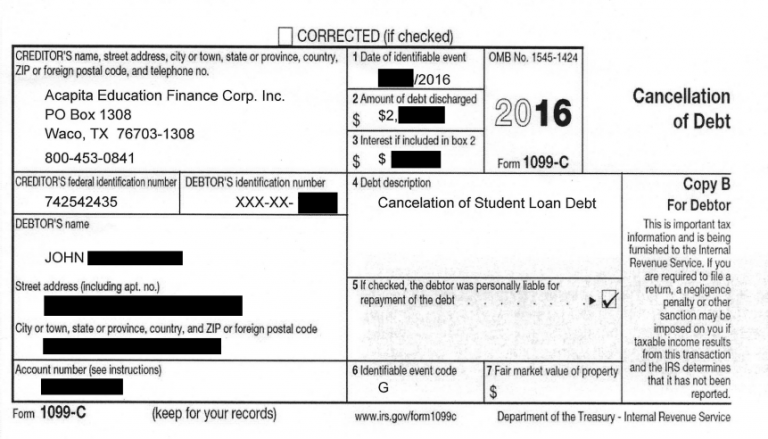

More Student Loan SPC Discharge win:

Secured Party Creditor: Rights & Remedies

One of the advantages of being a Secured Party Creditor is asserting your right as one of “we the people” of one of the united States of America — the constitutional republic. The people have rights under common law and equity.

The “property” 14th amendment citizen/slaves who were created with Birth Certificates and who have not discharged their birth certificate/slave status to become a national/secured party creditor again, do not have rights under common law and equity.

As one of the people, the grantors and beneficiaries of the constitution, you have a right of equitable relief because when the government took the people’s property and gold away in 1933, via House Joint Resolution 192 and the “National Emergency” Act, the people can assert the right to equitable relief.

When the government took the property, labor, and money of the American people, the American people became “Creditors” in a Creditor/Debtor legal relationship.

If a Creditor is owed money from the Debtor who borrowed money, according to UCC and Creditor/Debtor law, the Creditor can assert the right to a Set Off of the Credit owed to it. When this is done, there is no checks, bonds, money orders, or promissory notes required, nor should there be if you overstand what I just explained.

A 14th amendment slave/citizen who has been “granted” privileges by the government still has a noose around his/her neck. The government can change the rules on you at any time and set up other restrictions — and not even tell you what they are.

They can lie, cheat, and steal from you — and you have no rights because you are owned by them. You are not a “Creditor” if you are still assuming the diplomatic and tax-status role of the U.S. Citizen.

A U.S. Citizen is a surety for the corporate fiction, in contract with the de facto government to form a PUBLIC TRUST (ens legis “Strawman”). This makes you, the living man or woman, fully liable as surety for all debts. Your body, property, money, and offspring are collateral for a security agreement.

If you default on your debt, your money, property, and even your children can all be “Repossessed”.

Despite big powerful corporations able to imprison and enslave it’s slaves, you don’t have to consent to being a slave, instead you can break free by becoming a Secured Party Creditor. Since all their slave-status fraud was done without full disclosure — and fraud — when you were a minor and incapable of contracting in sound mind, you can at any time declare this contract fraud.

If you plan to still use the ALL CAPS NAME (because you plan on using currency, registering property, etc.), then you need to come up with some way to explain why you have been and will still be using this name.

You need to re-organize the ALL CAPS TRUST NAME, restructure the terms and roles, and remove the government and its agents from managing or administering your trust.

This is the point of having your initial trust meeting, appointing your beneficiaries, sending them notice, and then at the very end sending the Secretary of State in your Birth State, and Washington D.C. (who registered your birth to create the Strawman TRUST), so that you can give them notice to cease and desist, and to govern themselves according to your new sovereign position.

For a video and article covering this topic in more depth, go here:

understandcontractlawandyouwin.com/spc-webinar-replay/

Back to asserting rights to discharge — there is much information online about a variety of possible misinformation: writing your own bonds, checks, money orders on what people claim are alleged “strawman bank accounts” with various combinations of routing and accounting numbers. Many have gone to jail because the government claims they don’t exist — including Tim Turner, Brandon Adams, and Gordon Hall from Creditors in Commerce, who were convicted for trying to pay a tax debt with their own “money orders.” I highly recommend staying away from these failed methods.

Others try to pay/discharge their debts with “promissory notes,” which does not make any sense because any note with a fake promise is not legitimate. Besides, why do you need to “pay” anything if you already have Credit on account that you can use to set off?

We have covered this at length in our other materials, explaining exactly why these other processes do not work and are possibly very dangerous. If you are signed up to our announcement list and are a member of our Status Correction Course, then you get private/premium webinars going into detail, and a lifetime membership for updates.

Now there may not actually be “Credit” because the government overspends money it doesn’t have — so they did not create literal “bank accounts” for us to use — however they do have an obligation to allow us to discharge our debts.

From our point of view, based on consistent experience of successes, the way to discharge a student loan successfully (or any other discharge remedy) is to become a Secured Party Creditor and then assert the right to discharge.

Therefore you must be one of “we the people,” a national of one of the united States of America — and not OF THE UNITED STATES OF AMERICA. To understand the difference, read the free PDF “Cooperative Federalism”.

If you are going to discharge a federal student loan or other federal debt, you will never be able to get any federal benefits again — no more student loans, unemployment, federal aid of any kind, etc. If you read the Supreme Court case Hale v. Henkel, you will see that you give up your freedom and sovereignty when you take a federal benefit anyway.

It is also possible you will not be able to get a federally-insured mortgage loan to buy a home, and since almost all mortgages through financial institutions today are FDIC insured, you may be blacklisted with them also.

If you are an employee or contractor with a financial institution or federal government and you wish to discharge your debt with them, they will probably terminate your contract.

You cannot have your cake and eat it too. These concepts are not new — you cannot bite the hand that feeds you, and in this arena that is absolutely true.

There are several other websites selling similar things that we do, or at least mere “promises” of what we can actually do.

More and more people are coming to UCL instead because they see, sense, or feel that we are a company of integrity and transparency — and we live by the motto “at first, do no harm.”

I would rather maintain your relationship by cautioning you and have many choose not to do our process — and possibly refer someone out of appreciation for our honesty months or years later — rather than lie to you to get your money right now.

So just make sure you are comfortable with the above disclaimers. If you have any clarifications, let your UCL consultant know.

Again, to do the debt discharge process you need to first become a Secured Party Creditor. This involves waiving and clarifying that you are a citizen of your state republic — such as the “California” republic — and NOT “UNITED STATES.”

Please read the free PDF you can find online called “Cooperative Federalism” for the most thorough and factual/historical basis on the difference between being a state citizen and a United States citizen.

Also study what the United States Code says about the definition of “United States Citizen” — specifically at law.cornell.edu — 8 USC 1401. Other helpful sites:

These will assist you in seeing the conclusions that I have drawn — that you are NOT a U.S. Citizen unless you choose to make that declaration, and that you can also declare that you are not one at any time.

There are serious ramifications to officially declaring to the entire world and all government that you are no longer their subjects, property, or slave.

This is way larger than wanting to discharge your credit card and student loan debt. I do not accept clients who are looking to reduce or eliminate debt only. I only accept clients who truly wish to become sovereign because they know they are not U.S. citizens and who wish to live the rest of their life understanding and living out these legal concepts in congruency with the declarations they are about to make.

However, if you have determined that you truly wish to become a Secured Party Creditor, and then you want to discharge a student loan or any other debt as a bonus, we would love to help you with debt elimination.

Make Sure You Understand These Concepts

- Why are lawyers committing treason?

- What is the difference between a private citizen, state citizen, and United States Citizen?

- What is the Common Law? Please explain the distinction between common law and Statutory Law.

- Do non-U.S. citizens owe tax under the US Tax Code? Why?

- What is “positive law” and why is this significant?

I do not expect you to answer these questions thoroughly right off the bat, but you should be finding the answers to them and eager to understand them even deeper.

Do your best to research and explain the answers in your own words, and we will consider whether you are fit to become a secured party creditor — which entails waiving your US Citizenship.

This is important: if you move ahead with the process you will be signing affidavits under penalties of perjury declaring you are NOT a U.S. Citizen. The punishment for perjury is 5 years in prison. You must be able to understand and explain in your own words the summarization of any/all documents we prepare for you.

There is also a book called the Redemption Manual — a free PDF online you can read, which will give you quite a bit of study material to further immerse you in the subject matter.

A lot of people get so excited and wish to tell all their friends and family. I highly caution you to NOT share this material with those who are not ready — they will think you are crazy and may stir up trouble. You have to be very cautious and only introduce the most open-minded people to this.

When people search this technology online, they will find government websites saying this is a fraud or a scam. There are a lot of scams out there and those websites are overgeneralizing. Obviously they will use any example or excuse to dissuade people from moving forward with a process this powerful.

So you don’t want to tell people who cannot discern, who are not on the ascension path, or who will instantly believe anything on a government website.

Besides, if everybody discharged their debt and nobody paid their loans, many people would be out of work and the government would receive less in taxes — so obviously they do not want you to do this.

I have even known of people being visited at their home by the FBI, asked what a sovereign is, who gave them these documents, and whether they understand that filing such paperwork could be considered fraud. Others in prison with this literature have been placed in solitary confinement.

If it was not that powerful or effective, they would let prisoners have and distribute as much of this material as possible.

Now, the chance is probably only 1 in 5,000 that you might get a visit — and if you do, it is probably harmless. But I wish to warn you there is some small chance.

There are thousands of people becoming Secured Party Creditors every single month, and you have every lawful and legal right to do it. In fact, if you are a full-fledged Secured Party Creditor and you ever wind up in some trouble, you have a foundation of paperwork to protect you.

So my argument is that if you are someone who does not wish to just fold over and does not like being intimidated or punished when you have done nothing wrong, then becoming a Secured Party Creditor is definitely a serious option for you. It gives you armor of protection — and this is one of the key reasons people choose to become an SPC.

These are just some things to ponder when thinking about wanting to discharge any debt, especially a federal debt like a student loan. You should expect to be blacklisted and refused any federal benefits going forward.

Most Secured Party Creditors are able to avoid all withholdings from their paychecks and have many more tax advantages by using their trust as an asset protection trust — taxed as an irrevocable trust rather than as a U.S. Citizen/Strawman Trust.

The financial advantages of becoming a Secured Party Creditor are certainly significant. Almost all of our clients wind up paying taxes differently — by preventing their U.S. Citizen from “receiving” any income, closing all its bank accounts, ceasing all its contracts, and replacing it with their EIN number trust instead. The proper tax form to file is a 1041 for an irrevocable trust.

Hiring an accountant for the first year is highly recommended. Reading a basic accounting book within the first year will also be very helpful so that you can instruct your accountant accordingly.

You would basically be running your TRUST like a business with expenses and deductions. If your TRUST makes no profit, you could even file a $0 tax return on your 1041 at the end of the year. If you get audited, you show all your bank records and receipts and you will win. It is much better for a business or trust to get audited than you as an individual.

One more afterthought: if you discharge a loan, your credit report is going to be damaged for a long time. Do not count on using it to apply for other credit cards, loans, or mortgages for a long time. Yes, you can do credit repair and clean up negative info on your report — but that is not part of the package we offer.

In Conclusion

If you are just looking for “Debt Relief” to help “pay bills,” then our organization UCL is not for you.

But if you have been leaning toward becoming an SPC anyway — with the will and intent to take control and sovereignty over your own LEGAL NAME/BIRTH CERTIFICATE NAME for all the correct reasons (avoiding court, protecting assets, controlling your estate, abandoning the SSN contract) — then and only then will it be appropriate to talk about discharging your debts with the HJR 192 process.

Please make sure to read the Secured Party Creditor process page to learn more — these results are only possible as an SPC.

If you become an SPC with our program, we can then consult with you further about success and protocol with discharges.

to talk to our friendly and helpful consultants.

EDU Courses & Lessons

If you’re looking to take advantage of the world’s best tools for sovereignty and freedom, you’ll want to engage with Tyler UCL as often as possible. You’ll gain real clarity on your next steps in just one hour of legal mentorship and life coaching, and you’ll develop a true ally who is not only a genius, but authentic, emotionally vulnerable, and genuinely wants your friendship. In life, we all learn that we cannot succeed alone.